for expert insights on the most pressing topics financial professionals are facing today.

Learn MoreLet’s start with some brutal truths about college costs and their impact on families.

Image links to source.

Image links to source.

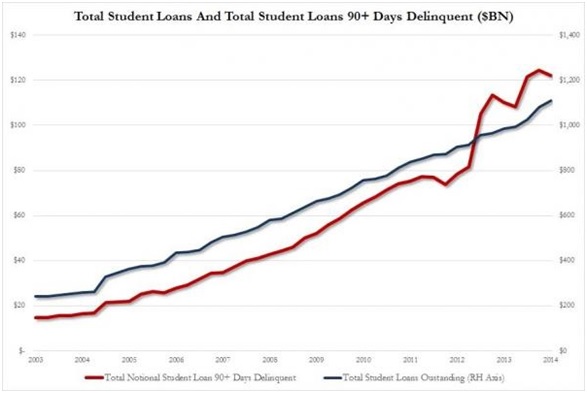

Source: The Wall Street Journal

Consider these additional facts:

In light of these brutal truths: the cost of college; the significant amounts of resources required to cover them; the inability for most families to save amounts necessary (confirmed by the increase in debt financing); and the effect on upper-middle-income families has changed the dynamic of college planning and its impact on retirement savings. According to a 2013 Sallie Mae report, here’s how parents attempt to balance paying for college and funding retirement: 50% are focused on college savings, while 60% are focused on retirement. With this overlap, 74% of parents said they’ll use retirement savings to pay college costs.

Parents want to provide for their children’s college education. To many parents it is a deeply emotional need, which means that when the time comes and it’s a question of saving for retirement or helping pay college costs, the more emotional and urgent need of college funding supersedes retirement savings decisions. They want happy, successful children, but they’re feeling the squeeze of paying for college while keeping retirement planning on track.

Unlike in the past, a singular focus on savings strategies doesn’t meet all the needs of families and doesn’t acknowledge or address the possibilities that exist for the client to reduce their total out-of-pocket college costs.

The rapid change in the college cost and funding landscape over the last 20 years has necessitated a new college planning paradigm for financial advisors. [inlinetweet prefix=”” tweeter=”” suffix=””]Today, consumers want and need more than just college savings strategies from their advisor.[/inlinetweet] They want their advisor to help them identify ways to reduce their out-of-pocket college costs – without compromising their retirement savings goals.

Advisors today who have a specialized capability to provide college savings plans AND college cost reduction strategies have a tremendous opportunity. They are positioned to differentiate themselves from other advisors, deepen the client relationship, generate more revenue and identify other opportunities with the client.

Beyond these, many advisors have a vested interest in helping clients avoid transferring tens and possibly hundreds of thousands of dollars of assets under management to cover college costs.

Next month we’ll look at four areas where a knowledgeable advisor can offer significantly more value for college-planning clients and help them reduce their out-of-pocket college costs.

This is the first in a series of articles on the eMoney blog by Roger Lorelle of Collegiate Funding Solutions (CFS), an eMoney partner. You can learn more about CFS on eMoney’s Partners Page or by visiting their website.